Subscribe to Our Newsletters

Feedstuffs is the news source for animal agriculture

Trends in response to climate change, animal production capacity and diseases such as avian influenza and African swine fever.

December 7, 2023

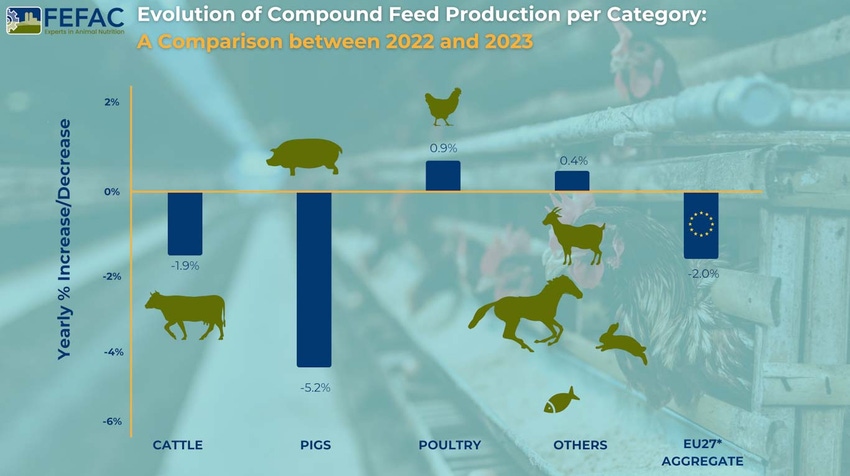

EU compound feed production (EU27) for farmed animals in 2023 is estimated at 144.3 million tonnes, reflecting a 2% decrease compared to 2022, according to data forecasts rovided by FEFAC members. The EU feed market in 2023 reflects continued political and market crisis management pressures and a growing demand for providing sustainable feed solutions to address market dynamics and regulatory considerations.

These trends are a response to the adverse impacts of climate change and animal diseases on the supply of raw materials, such as droughts and floods, and on animal production capacity, including avian influenza and African swine fever. Additionally, national policies ranging from greenhouse gas reduction goals to nitrate emission regulations, have contributed to these shifts.

Moreover, shifts in production methods, as well as reduced or shifting demand due to changing consumer preferences (the impact of food price inflation), are affecting compound feed production differentially across member states. While countries such as Germany, Ireland, Denmark and Hungary have witnessed approximately a 5% decline in feed production, other countries like Austria, Bulgaria, Italy and Romania, have experienced a modest increase. The remaining member states have either marginally decreased their feed production or maintained it at a level similar to the previous year.

Similar to 2022, the pig feed sector was most severely affected in 2023, experiencing a further decline of almost 2.5 million tons. Germany, for instance, faced a reduction in pork production due to the loss of Asian export markets and was targeted by negative media campaigns. Denmark witnessed a substantial drop of -13.6% in pork production in 2023. Spain, the largest EU pig feed producer, lost 800,000 tonnes of production due to shifting consumer preferences (food price inflation) and the loss of export markets. Meanwhile, Italy continued to grapple with challenges posed by ASF.

Poultry compound feed production in 2023 displayed a more positive trend, with production increasing by 0.9 million tons compared to 2022 as some countries were recovering from avian influenza impacts in 2022. However, both Hungary and Czechia faced further production decline, attributed to a decrease in poultry broiler production, resulting in gaps in rotations and presenting challenges for local slaughterhouses. It must be highlighted that modest growth is not sufficient to recover from losses in 2022, meaning 2023 tonnage will still be 700,000 tonnes below 2021 levels.

Cattle feed production in 2023 experienced a decrease of 0.8 million tons compared to 2022. Similar to Spain, Portugal faced water scarcity issues leading to farm closures, particularly in ruminant sectors. Challenges such as low milk prices and cattle diseases further affected the industry. In contrast, cattle farmers in Czechia and other Central and South Eastern European countries benefited from sufficient grass growth, leading to reduced demand for industrial cattle feed.

Regarding the outlook for compound feed demand in 2024, the scenario remains uncertain. Key factors, such as the impact of animal diseases, economic uncertainty, persisting high food price inflation, ongoing weather irregularities, and the increased imports of poultry meat products from Ukraine, are affecting local production. The influence of "green and animal welfare" policies is expected to adversely impact the market outlook for livestock and feed production, although costs for key feed materials, mainly feed cereals, have fallen back to levels before the Russian invasion of Ukraine.

You May Also Like

Enter a zip code to see the weather conditions for a different location.